Half a century ago, eight multinational corporations wandered into a Malaysian swamp and began making demands. They wanted stable electricity and predictable customs. They needed clean water in industrial quantities and a workforce capable of operating inside process tolerances unfathomable to most of the world. The swamp obliged. Bayan Lepas became a Free Industrial Zone, then an ecosystem, then … an accumulation of institutional memory so dense that it now is infrastructure. The original eight—Intel, AMD, Hewlett-Packard, and their peers, known locally as the Samurai Eight though the rosters blur at the edges—did not arrive from loyalty, but because the village could be shaped for less than the cost of building elsewhere. What they left behind is an armory: a place where silicon gets mounted, balanced, tested, and certified for deployment. The armory smells of nothing, and sounds like filtered air and the hum of laminar flow. Its warriors wear bunny suits, and its blades are invisible to the naked eye. Yet the path to the armory door still runs through mud, and the river outside is rising.

Taiwan operates the forges; ASML supplies the fire. Malaysia finishes what the forges produce. Packaging and testing once resembled credits rolling after the film ends, but physics has rewritten the hierarchy. When the corridor for smaller transistors narrowed to the width of a few atoms, performance gains migrated from lithography to assembly. Chiplets, interposers, and 3D stacks—the craft that translates laboratory silicon into deployable systems—now live in the finishing shop. The armorers discovered, slowly and then all at once, that they were no longer peripheral. A katana fresh from the forge is potential energy; it becomes kinetic only when hilted, balanced, and matched to a warrior’s reach. Malaysia holds the hilts.

The question is whether the crossing to reach those hilts will remain passable, or will the bridges under construction downstream—cheaper fords in Vietnam, subsidized channels through India, faster currents in China—redirect traffic before the armorers can upgrade their craft?

The Swamp that Prints Tolerance

A place becomes a craft long before it becomes a headline

Penang’s origin story is not one of magic, but of compounding. The Bayan Lepas Free Industrial Zone emerged in the early 1970s as a deliberate speculation on export manufacturing, anchored by multinationals whose demands forced an ecosystem into existence. Intel arrived. Hewlett-Packard arrived. Others followed, and their specifications—stable power within tolerances tighter than the national grid had ever promised, water purity that the local utility had to learn to deliver, customs routines that could not tolerate unpredictability—became the curriculum for an entire regional economy. The village did not have these capabilities when the samurai appeared. The village acquired them because the samurai would not stay otherwise. Decades later, the capabilities remain even as the original names have merged, spun off, or reorganized beyond recognition.

The ecosystem that resulted is disproportionately concentrated in assembly, packaging, and testing. Malaysia accounts for roughly thirteen percent of global semiconductor ATP and ranks among the world’s top semiconductor exporters. The figures require careful handling—approved investment differs from cash deployed, export share differs from value-added share—yet Malaysia is not a factory, but a tuning shop. The wafer arrives as theoretical performance, a pattern etched in silicon that has never met the outside world. The shop introduces that pattern to thermal stress, to mechanical vibration, to the thousand small indignities of deployment. What survives the introduction ships. What does not gets sorted, binned, or scrapped before it can embarrass anyone.

The 2021 auto-chip shock demonstrated what happens when the shop closes.

The shortage was never a shortage of wafers; fabs continued to produce. It was one of finished, tested, packaged components that could be inserted into a vehicle’s wiring harness and trusted to function for a decade. Procurement offices that had spent years squeezing suppliers for marginal cost reductions discovered that the marginal supplier was also the critical path. AlixPartners estimated the revenue impact on global automakers at roughly $210 billion—a figure imprecise in its accounting yet precise in its lesson. The armory had seemed peripheral until it closed, and then nothing else mattered.

Malaysia’s role is sometimes expressed as electrical and electronics comprising forty percent of exports, sometimes as a GDP contribution figure, sometimes as a share of global semiconductor trade. These are not interchangeable metrics, and treating them as such invites confusion. The safer frame is functional. Malaysia is where silicon becomes product: tested, certified, shipped.

The armorers do not forge the blades—they make sure that the blades cut.

The village learned this craft over fifty years, one transnational specification at a time. Its knowledge is embedded in customs routines that process semiconductor shipments without delay, in utility infrastructure that delivers power within tolerances most grids cannot promise, in a workforce that understands cleanroom discipline as a daily practice rather than an occasional imposition. The swamp is gone. The tolerance it learned to print remains.

The Back End Became the Fuse Box

When transistors slow down, geometry moves to the package

For years, packaging occupied the unglamorous end of the semiconductor value chain. The excitement lived upstream, in lithography and transistor density, in the race to shrink features to dimensions that required new physics to describe. Packaging was where the race ended and the paperwork began: mount the die, wire the bonds, seal the package, ship the box. Then the race stalled. Moore’s Law did not repeal itself, yet the corridor narrowed. Each new node cost more, yielded less, and delivered diminishing returns in performance per dollar. Industry leaders discovered that they could no longer shrink their way to victory.

They needed a new geometry, and it lived in the package.

Chiplets, 2.5D interposers, and 3D stacking shifted performance gains from transistor size to transistor arrangement. The interposer becomes a chessboard; the chiplets become pieces that can be mixed, matched, and upgraded independently. The performance bottleneck moved from how small to how connected. Heat dissipation, signal integrity, power delivery—these became the limiting factors, and they are all packaging problems. The armorers who once applied finishing touches now determine whether the system performs at specification or throttles itself into mediocrity.

Intel’s Malaysia investments mark the clearest evidence of this shift. The company has repeatedly described its Malaysian facilities as the location for its first overseas advanced packaging operation, explicitly tied to Foveros technology and 3D integration. Subsequent announcements added hundreds of millions of dollars in expansion, framed as demand-driven responses to packaging and test capacity constraints. Intel is not investing in Malaysia to perform the same work cheaper, but to perform work that did not exist a decade ago. The armory is acquiring new tools, and the new tools are not optional.

The constraint matters for AI infrastructure specifically. The chips that power large language models and training clusters are not single dies; they are systems-in-package, assemblies of compute, memory, and interconnect that must be integrated with precision the forge cannot provide. Advanced packaging is increasingly discussed as a bottleneck on AI deployment—not the silicon itself, yet the yield, the thermals, and the bandwidth that determine whether silicon translates into operational capacity.

Malaysia’s role resembles a switchboard operator during a storm. The generators upstream produce electricity; the switchboard decides which circuits stay lit. A thirteen percent share of global ATP sounds modest until you recognize that the percentage represents not volume but leverage.

The armory does not control how many blades are forged, only how many reach the battlefield ready to cut.

The back end of the semiconductor supply chain has become the fuse box for the front end’s ambitions. When AI demand outstrips packaging capacity, the queue forms in Malaysia, in Taiwan’s backend facilities, in the handful of locations where advanced assembly is possible. The wait is not for wafers; the wait is for integration. Physics forced this inversion, and physics will not reverse it. The transistor race continues, yet the trophy now goes to whoever can mount the most transistors in the tightest space with the best thermal management and the fastest interconnects. The armorers have become kingmakers, though kingmakers who must still cross the river each morning to reach their stations.

The Breach in the Wall

Armorers who leave take more than their labor

Every siege finds its breach point, the section of wall where pressure concentrates until stone begins to crack. For Malaysia’s semiconductor ecosystem, that breach is talent. Factories do not emigrate. Engineers do. The armory’s accumulated advantage—decades of process knowledge, tolerance intuition, yield optimization learned through error rather than instruction—lives in people who can resign. When those people leave, they carry judgment that no training program can replace.

The breach is silent, incremental, and visible only in hindsight, when the line that once ran at yield begins to stutter and no one remaining knows why.

The gradient runs toward Singapore, where the wages are higher and the career paths are denser. The credential portability of a concentrated city-state creates gravitational pull that no neighboring country can match. A Malaysian engineer in Penang can see the Singapore skyline from certain vantage points; the flight takes less than an hour, and the decision to leave takes less than a month once the offer arrives.

The cohort that matters is not fresh graduates, who can be trained, nor senior executives, who can be recruited from global talent pools. The breach opens in the middle: mid-career engineers who spent a decade learning what the specifications do not say, who know which machines drift and which operators compensate, who carry process maps that exist nowhere on paper. This layer leaks fastest and replenishes slowest.

Malaysian policymakers understand the problem in outline. The National Semiconductor Strategy treats workforce upgrading as an explicit priority, and the government’s $250 million agreement with Arm over ten years aims to build training infrastructure and ecosystem capability. The numbers are easy to announce and difficult to audit.

Trained engineers do not automatically become retained engineers, and training pipelines address entry-level supply rather than mid-career attrition. A new graduate can learn to operate a machine; learning to feel when the machine is preparing to misbehave takes years of scar tissue. The policy apparatus is building barracks while the veterans weigh offers from armies that pay better.

Singapore’s pull is not solely compensation, though compensation matters. The compression of a city-state creates more career possibilities than Malaysia’s geography can replicate:

- employers within commuting distance

- lateral moves possible without relocation

- network density that compounds individual reputation

An engineer who leaves Penang for Singapore does not merely earn more; that engineer enters a denser lattice where the next opportunity is always visible. Malaysia’s counteroffers—cost of living, quality of life, the intangible pull of home—are real yet diffuse. They do not appear on a pay stub. The armorers weigh tangible against intangible and make rational decisions, one resignation at a time.

For investors tracking firms with Malaysia exposure, the talent constraint surfaces through operational signals that precede earnings revisions.

Cracks appear first as longer waits for specialized hires, then as bidding wars for the smiths who remain, then as announcements of apprenticeship programs that confess the obvious: master craftsmen are leaving faster than new ones can be made. Hiring timelines extending in packaging and test roles, wage inflation outpacing regional benchmarks, training facility announcements that paradoxically signal inadequacy—these are the fractures that can be monitored before they widen into guidance cuts. The armory’s interior remains sterile, climate-controlled, humming with laminar discipline. Its vulnerability is not the machines.

Its vulnerability walks out the door each evening and sometimes does not return.

Neutral Ground Is Prime Real Estate

Supply chains pay for places that do not force a binary choice

Geopolitics has pushed procurement into a posture the textbooks never anticipated: duplicate, do not optimize. The headline version is “China+1,” yet the deeper logic is institutional. Companies will pay for optionality—second sites, diversified logistics, jurisdictions that reduce the probability of being trapped by sanctions, export controls, or sudden compliance shifts. The premium is not for novelty, but for continuity. A half-century ecosystem is itself an asset, one that cannot be conjured by subsidy alone. Suppliers know the customs routines. Engineers know the process tolerances. Regulators know the industry’s rhythm. When a multinational needs to reroute capacity in a hurry, it does not want to teach a new village how to meet specifications. It wants a village that already knows.

Malaysia offers neutral ground in both senses of the phrase: a jurisdiction that does not force a binary geopolitical choice, and a power infrastructure that can deliver the electrons such choices require.

Malaysia’s pitch rests on this accumulated credibility. The National Semiconductor Strategy frames upgrading as the path forward. The aim is to modernize ATP into advanced packaging, growing capabilities in power semiconductors and building local design capacity. The money trail confirms the intent, even if approved investment differs from deployed capital.

Two anchors illustrate the pattern. Infineon has made Kulim a centerpiece of its silicon carbide expansion, describing a phased path toward a world-scale 200mm SiC power fab; the construction site sits on land that was plantation a generation ago, red earth graded flat and drainage channels cut to keep the water table from reclaiming what the jungle surrendered. Nvidia and YTL have been tied to a multi-billion-dollar AI data center buildout in Johor. Subsequent reporting indicates that a facility powered by high-end Nvidia systems has been commissioned. Its cooling towers hum in the humid air, drawing megawatts from a grid that stretches back through substations and transmission lines to generators burning what the world is trying to stop burning.

The crossing is muddied, yet still passable.

Companies fording the river here commit to a path not easily reversed. Malaysia’s value is that it knows the bottom. Decades of institutional memory are encoded in the pilings sunk through swamp, in the cables strung across rivers, and in the customs protocols that clear shipments while neighboring ports still shuffle paperwork. Neutrality is not a moral stance, but a commodity. The ability to keep shipping while two superpowers redraw the rules mid-game commands a premium that shows up in approved investment figures, facility expansions, and the quiet decisions of procurement officers who need optionality more than they need the lowest unit cost.

Taiwan is too exposed; a single missile closes the strait. China is too entangled; export controls multiply by the quarter. The United States is too expensive; labor and permitting costs stretch greenfield projects across a decade. Malaysia is just right; it sits at the sweet spot between these constraints, close enough to ship, distant enough to survive, familiar enough to trust.

Optionality, however, has a price denominated in electrons.

Semiconductors are energy-dense manufacturing; AI data centers are energy-dense demand. Malaysia’s competitive set now includes its grid, not only its tax incentives. The national power mix remains fossil-heavy—coal and gas dominant, solar still small—and grid upgrades plus renewable buildout are central to sustaining investment from multinationals whose procurement systems now include sustainability fields that can block purchase orders.

The constraint is not reputational, but operational.

Advanced fabs require voltages that do not drift. AI clusters require megawatts that arrive without interruption. Tenaga Nasional has committed tens of billions of ringgit to transmission and distribution upgrades, a figure that signals where the bottleneck binds. The substations being built sit on the same terrain the original samurai crossed: drained swamp, graded earth, humidity that corrodes what is not maintained. The neutral wire still carries current from coal. The ground beneath the armory is not yet clean.

The Johor AI buildout becomes a template when viewed through this lens. It is a preview of the terms hyperscalers will increasingly demand: power, land, and permits packaged together, a turnkey crossing where the mud has been paved and the footing guaranteed. Competitors with shakier grids offer cheaper labor yet cannot promise megawatts alongside square meters.

Vietnam’s infrastructure gaps show up in procurement risk models as probability-weighted delays. India’s permitting timelines show up as carrying costs that erode the subsidy advantage. Malaysia’s grid is imperfect, its generation mix is dirty, its transition is measured in decades rather than quarters—yet the electrons arrive, and arriving is what matters when the alternative is building your own substation. The armorers who remain in this village are betting that the grid will keep pace with their ambitions.

If it does not, the fords downstream will look more attractive, and the crossing here will silt up with the debris of projects that never commissioned.

The Window Narrows Even When the Headlines Widen

Malaysia is racing two neighbors and one internal clock

Vietnam can be cheaper. The procurement spreadsheets prove it: line items for labor, utilities, and logistics that undercut Penang by margins wide enough to trigger sourcing reviews. India can subsidize harder. The Production Linked Incentive schemes write checks that Malaysia’s treasury cannot match, and the domestic market behind those checks is vast enough to justify localized production. China can scale faster. Factories rise in months, supply chains materialize as if summoned, and the density of manufacturing expertise compresses timelines that elsewhere stretch into years. Taiwan can be more advanced. The most sophisticated lithography on earth operates there, guarded by mountains and the implicit threat of a conflict no one wants to price. These are not abstractions in a strategy document; they are pressures the armorers feel against the walls, vibrations carried through the ground, the sound of hammering from rival villages that have decided they too want samurai.

Malaysia’s edge is that it is already in the loop—qualified, shipping, trusted.

The village does not need to prove it can meet specifications. It has been meeting them for fifty years. Yet loops can be bypassed. The road through the village is the fastest route only until a faster road opens elsewhere. Vietnam’s labor arbitrage is real, even if its grid stutters and its engineering talent pool runs shallow. India’s subsidies are real, even if its permitting apparatus moves at a pace that makes procurement officers price in delay. China’s scale is real, even if its geopolitical entanglement disqualifies it for customers who need supply chain separation. Each competitor carries a limitation, yet each limitation can be overcome with enough time and capital. The question is not whether alternatives exist, but whether they mature before the village can upgrade.

The road through the village remains busy, for now. Travelers take it because the footing is known, the tolls are predictable, and the bandits have been cleared. If the village keeps improving the road—adding lanes, smoothing ruts, building shelters where travelers can rest—traffic will continue. If the village lets the road deteriorate while competitors pave their own routes, travelers will reroute quietly, one caravan at a time. No battle, no siege, no dramatic defeat will precede the thinning of the traffic as the village elders realize the road is empty and the travelers have found another way. The armorers are not defending a fortress; as much as maintaining a thoroughfare.

The work is unglamorous, continuous, and fatal to neglect. What does maintenance look like in terms an investor can monitor? The signposts are operational, not rhetorical:

- Advanced packaging capacity utilization at Intel’s Malaysian facilities, tracked through earnings commentary and capital expenditure guidance

- Power semiconductor project milestones at Infineon’s Kulim site, visible through press releases and industry conference presentations

- Design-win announcements from Malaysian R&D centers, indicating that the ecosystem is climbing from assembly toward architecture

- AI infrastructure commissioning timelines in Johor, signaling whether the grid and permitting apparatus can keep pace with demand

- Hiring velocity in specialized roles, revealing if the talent pipeline is filling or draining

These are the metrics that matter. The departure board tells the story before the annual report does. The armorers’ calculations precede the analysts’ revisions.

The samurai who wandered into the swamp a half-century ago did not promise loyalty; they promised results, and they stayed only as long as the village delivered. Their successors calculate the same way. The mud remains, churned by generations of crossings. The river continues to rise, fed by rains that fall whether the village is ready or not. The armorers stand at their stations, blades arriving from forges they do not control, and the only question that matters is whether the travelers will still be coming when the dry season ends—or whether the fords downstream will have opened, the bridges completed, and the road through the village left to the weeds and the silence that follows irrelevance.

Six Trades for the Muddied Crossing

Reconnaissance reports from the armory’s perimeter

CAVEAT EMPTOR: These slides are NOT financial advice. Rather, they are provided as proofs-of-concept. For convenience, the forward horizon is 18 months. For study purposes, the set is ranked by complexity of execution. Always exercise proper position sizing and a precisely defined risk management plan in any live trading. Never trade more than you can comfortably afford to lose.

U.S.-listed tickers offer liquidity and familiarity. Intel’s packaging strategy, Broadcom’s Penang logistics footprint, First Solar’s Malaysian manufacturing base, Nvidia-linked infrastructure: each represents a different angle on the arena. Traders in Singapore, Hong Kong, or Kuala Lumpur will find sharper, more direct instruments and expressions; the method transfers regardless of jurisdiction.

The trades that follow target liquid companies where Malaysia functions as a gear in the machine—enough exposure to matter, diversified enough to survive disruption.

Trade 1: Nvidia Volatility Trapdoor

Sometimes the cleanest way to express uncertainty is to rent it.

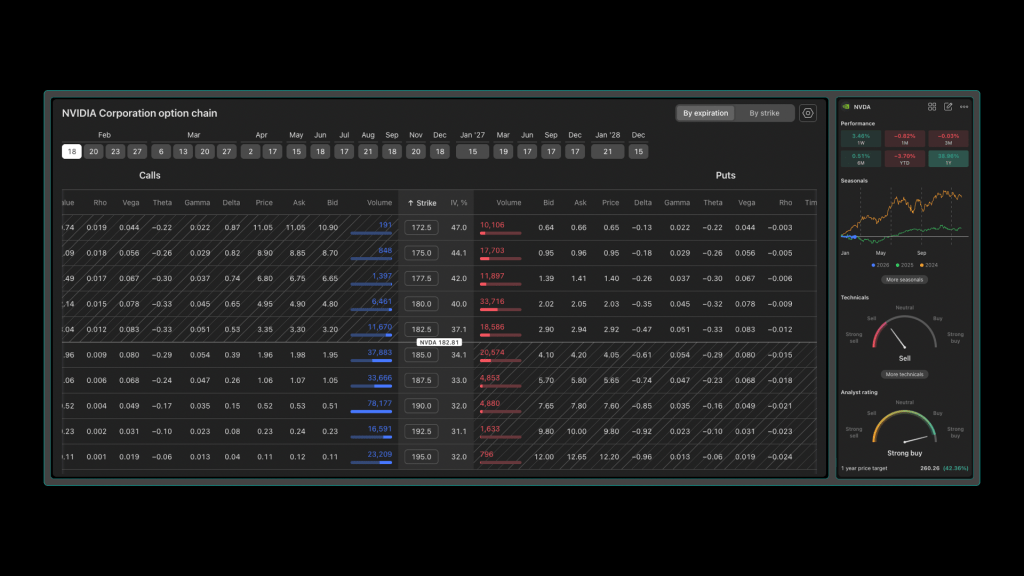

The technicals gauge reads “Sell” while analyst consensus reads “Strong Buy” with a $260 price target, a divergence that will resolve violently when new information arrives. The disagreement is itself a volatility catalyst. The market has priced a range; the catalysts will test whether it holds. The options chain shows positioning for a $175–$190 range, with call open interest clustering at $185 and $190 while put open interest concentrates at $180 and below. Implied volatility at the money runs around 37–40%, declining as strikes move further from current price in either direction. Seasonal patterns show 2026 tracking below the 2024 and 2025 paths through this window—underperformance relative to historical tendency.

Instrument: Nvidia Corporation (NVDA) options, delta-neutral long-volatility structure (long straddle or long strangle), initiated near at-the-money.

Thesis: NVDA has an earnings event scheduled for February 26, 2026, and GTC 2026 runs March 17–20—two high-attention catalysts inside a four-week window. When AI narratives crowd positioning, realized moves around earnings and roadmap events can exceed what the options market prices, especially if guidance language shifts from demand strength to delivery constraints. The unknowable is which datapoint—China controls, hyperscaler digestion, product cadence—becomes the narrative hook that forces repricing.

Catalysts and Monitoring: February 26, 2026: NVDA earnings (monitor IR webcast and transcript for packaging/supply commentary). March 17–20, 2026: GTC (monitor keynote messaging and product roadmap for demand signals).

Entry / Exit Logic: Enter ten to fourteen calendar days before earnings only if the stock is compressing (lower ten-day ATR versus thirty-day) and implied volatility is not already at a local extreme versus the last two earnings cycles. Take profits at fifty percent of premium value, or scale thirty/thirty/forty into spikes. Close remainder within seventy-two hours after GTC unless the move is still accelerating. Time stop: exit at twenty-one days to expiration regardless.

Invalidation: If NVDA breaks the pre-entry range and trends without retracing, cut the structure when loss reaches one R. If implied volatility expands sharply before the event without commensurate realized movement, the edge is gone; exit early.

Risk Management: Define one R as one hundred percent of premium paid. Cap premium outlay to 0.5 R of portfolio risk. Pair with Trade 2 if semiconductor beta is elevated.

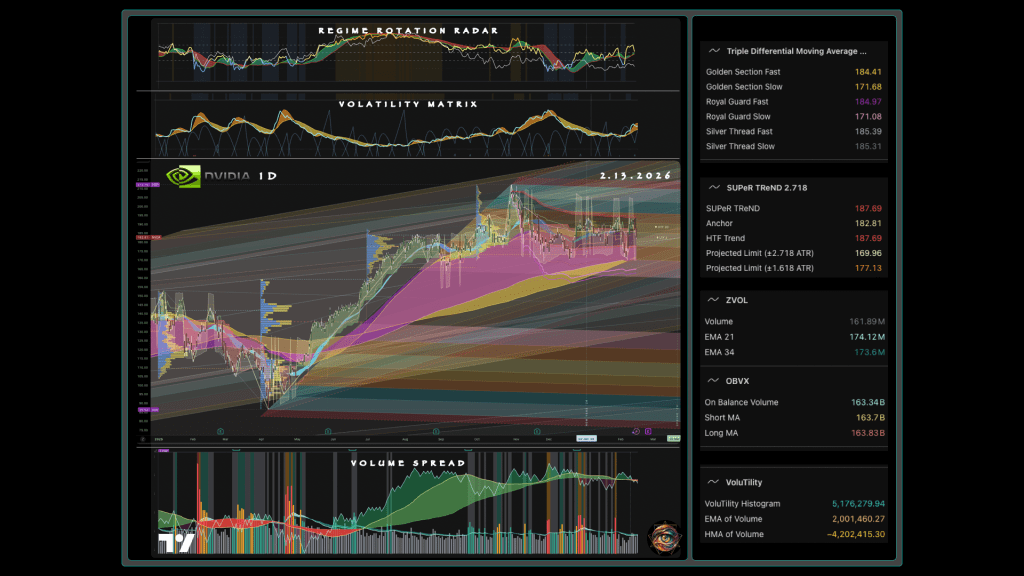

Price Action: Price has consolidated in a $165–$195 range since the January spike to $212, carving a shelf where neither buyers nor sellers have claimed victory. Overlapping pitchforks anchored to major swing points converge at current price, marking a decision zone where multiple structural forces collide. The Periodic Volume Profile places the current level at the Point of Control from Q3 2025—the price where the market found equilibrium during last summer’s consolidation. Overhead supply from the Q4 and Q1 volume clusters creates resistance that any rally must absorb before new highs become possible.

Volume Spread Analysis: Volume has run below average for weeks, confirming that the consolidation reflects hesitation rather than accumulation. On Balance Volume is flat, drifting sideways without the signature of institutional buying or selling. The ratio of up-volume to down-volume leans slightly bullish, yet the magnitude is too weak to signal conviction. This is a market digesting a prior move, waiting for new information before committing capital.

Volatility Matrix: The ATR ribbon shows compression: recent daily ranges are narrower than the prior month’s, a coiled spring awaiting release. The trend anchor sits exactly at current price, with resistance overhead at $187.69 and projected support at $177.13. A close above the anchor re-establishes bullish posture; a close below the lower projection confirms breakdown. The differential moving average braid has compressed to near-convergence, a condition that historically precedes sharp expansion in either direction.

Regime Rotation Radar: The RRR shows NVDA in regime transition: leadership lost, capitulation not yet arrived, the stock suspended in the indeterminate middle where directional trades fail and volatility trades thrive. The primary ratio, NVDA/QQQ, has faded from deep green dominance during the mid-2025 rally into contested amber-olive territory where neither bulls nor bears can sustain momentum. The z-score hovers near zero, confirming mean reversion rather than trend. The ribbon alternates between green and red in quick succession, each thrust failing before it can establish direction. The secondary ratio, NVDA/SMH, tells the same story: NVDA is no longer exceptional within semiconductors, merely a participant in sector beta rather than its driver. The regime color sits in lemon yellow—no directional lean, no momentum confirmation, the exact condition where straddles and strangles find edge. Ribbon chop at this level indicates that realized volatility is likely being underpriced by the options market, which has anchored to the recent compression. The market has repriced NVDA from “the AI stock” to “a semiconductor stock,” yet the options chain has not fully absorbed that demotion’s implications. The catalyst cluster will force the regime to declare itself, and the declaration—whichever direction it takes—will exceed the movement the current implied volatility anticipates.

Trade 2: Semiconductor Circuit Breaker

When correlations spike to one, insurance becomes alpha.

Semiconductors are underperforming both the broad market and tech specifically. The mix signals sector-specific stress rather than simple beta unwind. The cycle rests at an inflection point, suggesting a turning of the wheel rather than a pause within an existing phase. Momentum readings are not yet oversold, leaving room for further decline before mean reversion becomes probable. Bearish divergence is present, hinting that the decline may be maturing even as it continues. Directional movement is building. Conditions favor initiating protection now rather than waiting for cheaper premiums that may never arrive.

Instrument: VanEck Semiconductor ETF (SMH) options, explicit hedge via three-month put spread (buy near at-the-money put, sell lower-strike put).

Thesis: SMH is a highly liquid semiconductor ETF with heavy exposure to the AI-cycle names that dominate index leadership. If the Malaysia upgrade thesis is correct yet the cycle turns risk-off, the basket drawdown will arrive through sector beta first. A defined-risk hedge keeps the entire trade set solvent during correlation spikes.

Catalysts and Monitoring: FOMC calendar and macro releases (CPI, PMI) over the next three months. Semiconductor event cluster: NVDA earnings February 26, TSM monthly sales releases, and any export-control announcements.

Entry / Exit Logic: The ideal entry occurs when SMH is extended eight to ten percent above the fifty-day moving average and realized volatility is subdued versus the prior month. The current setup, with SMH already down twenty percent from January highs, suggests the optimal window for cheap protection has passed; initiate on any relief rally that restores complacency, or accept higher premiums now if portfolio exposure demands immediate coverage. Target protection through the most likely drawdown band, anchored to recent swing lows. Take profits if SMH approaches the short strike. Time stop: close at fourteen days to expiration if not working.

Invalidation: None required beyond defined risk; the premium is the cost. If the volatility regime is already stressed (VIX elevated, SMH already breaking down), wait for a bounce rather than overpay at peak fear.

Risk Management: Premium outlay capped at 0.5 to 1.0 R for the portfolio, explicitly offsetting correlation risk in Trades 4 through 6.

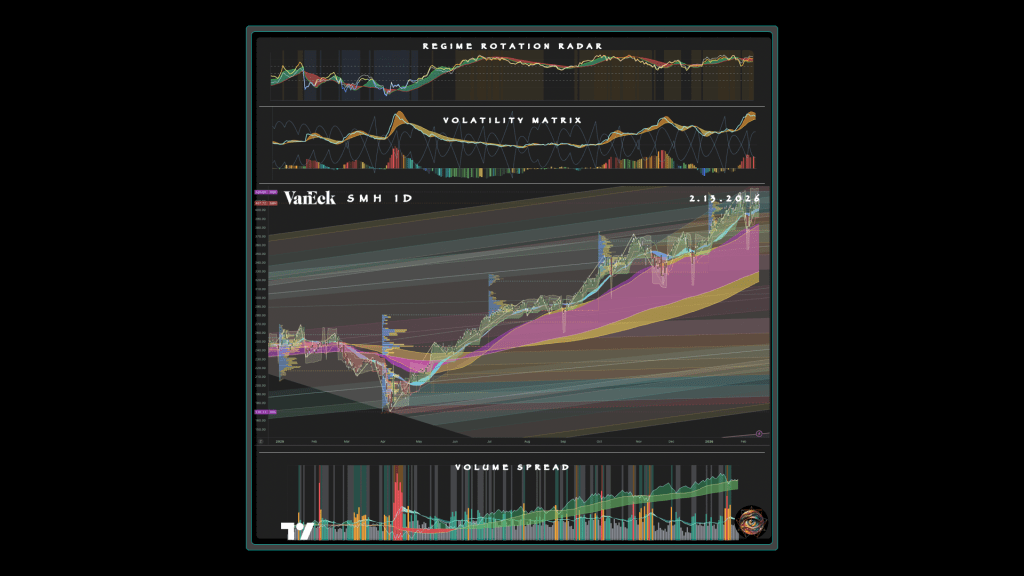

Price Action: SMH peaked near $420 in late January and has fallen over twenty percent to $333, slicing through the pitchfork channels that supported the rally from last April’s low. The magenta and teal structures that once cradled price are now ceilings rather than floors. The Periodic Volume Profile reveals a pocket of thin trading between the Q4 consolidation zone and current levels—price fell through air, which explains the velocity. What was support has become resistance, and the chart now reads as a downtrend until proven otherwise.

Volume Spread Analysis: Selling has come on heavier volume than the rally that preceded it, the signature of distribution rather than orderly profit-taking. Down-volume outpaces up-volume by nearly two to one in recent sessions, confirming that supply is overwhelming demand. The cumulative flow has turned negative and continues to deteriorate. This is not a pullback within a trend; this is a trend change announcing itself.

Volatility Matrix: Daily ranges have expanded as the decline accelerated, the opposite of the compression that characterized the January consolidation. The trend structure has flipped bearish, with the prior breakout level near $392 now acting as resistance. The moving average braid has fanned wide, a sign of momentum rather than consolidation. Price would need to reclaim $407 to negate the breakdown, a distance of over twenty percent from current levels.

Regime Rotation Radar: The RRR reveals a market in the early stages of regime change: semiconductors led higher through 2025, and now they are leading lower. The primary ratio shows SMH weakening against SPY at an accelerating pace, with momentum favoring the denominator rather than chopping indecisively. The ribbon has flipped from green to red and stayed red, the signature of sustained underperformance rather than noise. The secondary ratio confirms the stress is sector-specific: semiconductors are lagging tech, not merely participating in a broader unwind. The regime color has shifted from the amber of leadership through the yellow of indecision into early blue territory, though capitulation has not yet arrived. What the RRR makes visible is the correlation trap forming in real time: as SMH underperforms, its beta to the market is tightening rather than loosening. A hedge initiated now gains value not only from SMH declining but from the relationship itself intensifying under stress. The circuit breaker charges precisely when the current flows hottest.

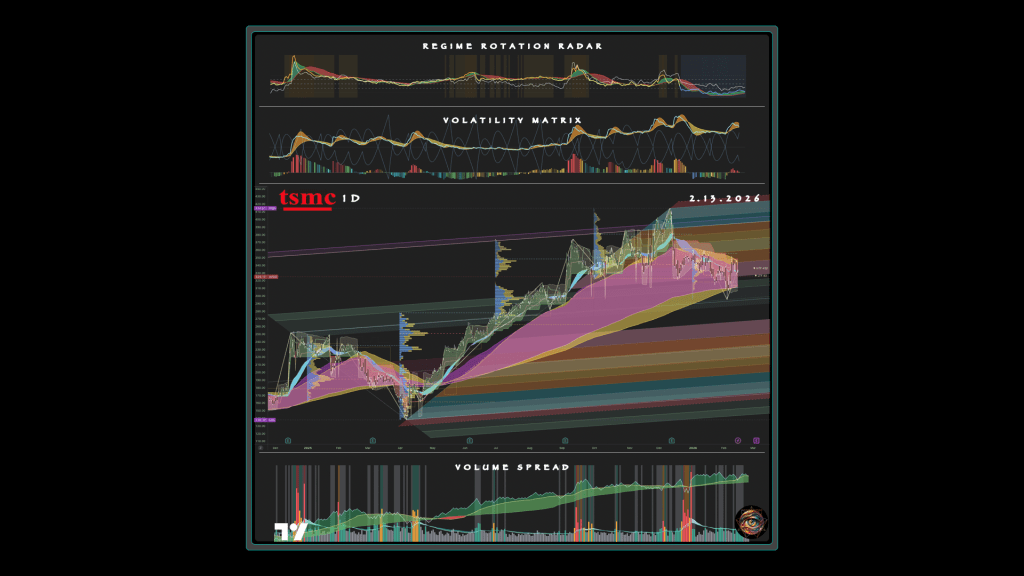

Trade 3: Taiwan Premium Mean Reversion

When the whole world buys the same bridge, tolls get priced to perfection.

Widening of volatility density in price action suggests that TSM may be earlier in its cycle than the broader market. Volume momentum has turned negative, an early warning that buying pressure is waning even as price holds. Trend has no strong directional bias—the stock is drifting rather than driving. The overall picture is a stock that has outperformed but is now resting, vulnerable to narrative shifts but not yet breaking down.

Instrument: Taiwan Semiconductor Manufacturing Company Limited (TSM), short equity or synthetic short via options.

Thesis: TSM’s next earnings window is mid-April 2026, and TSMC’s investor calendar shows monthly sales releases on February 10, March 10, and April 10. If AI demand narratives soften even slightly—customer digestion, delivery bottlenecks, margin pressure—the market can rotate from front-end perfection into names with different leverage. The trade expresses mean reversion on the TSM premium relative to the semiconductor basket.

Catalysts and Monitoring: February 10, March 10, April 10, 2026: monthly sales releases (monitor TSMC investor site). Mid-April 2026: earnings and guidance (monitor transcript for capex and margin commentary).

Entry / Exit Logic: Enter only if TSM/SMH ratio rolls over on the daily chart (lower high confirmed) and TSM breaks a prior twenty-day low after a failed rally. Avoid blind shorts into strength. Take partial profits at 1.5 R, cover the rest into 2.5 R or into earnings if already profitable. Time stop: three months.

Invalidation: Daily close above the most recent swing high (define that distance as one R). Monthly sales accelerate and earnings guide capex and margins higher—exit even if the price stop is not triggered.

Risk Management: Size smaller than longs (0.5 R maximum). Use Trade 2 as the correlation hedge rather than adding new legs.

Price Action: TSM peaked near $380 in early January and has pulled back to $366, holding up better than the broader semiconductor complex but no longer making new highs. The pitchfork structure from the April 2025 low at $134 remains intact, with price still trading within the upper channel, yet the angle of ascent has flattened. The Periodic Volume Profile shows price sitting in a well-traded zone from Q4, where buyers and sellers found equilibrium during the autumn consolidation. The HTF marker near $380 and LTF marker at current price suggest the higher timeframe trend is intact but the lower timeframe has stalled—a condition that precedes either continuation or failure.

Volume Spread Analysis: Volume has been unremarkable during the pullback, running near its moving averages without the spike that would indicate either panic selling or aggressive accumulation. On Balance Volume remains positive and stable, suggesting institutional holders have not yet begun to distribute. The PVP shows down-volume slightly exceeding up-volume at 150K versus 100K, a mild bearish tilt but not yet conviction. This is a stock holding its ground while waiting for new information rather than a stock under active liquidation.

Volatility Matrix: Daily ranges have expanded modestly, with realized volatility rising but not yet signaling panic. The trend structure remains bullish, with the trend line at $340 as support and the anchor at current price—price would need to break below $351 to trigger the volatility stop and confirm a trend change. The moving average braid remains fanned in a healthy configuration, with the fast threads above the slow, though the spread has narrowed as momentum decelerates. The projected limits at $382 and $365 bracket the current range, suggesting consolidation rather than breakdown—for now.

Regime Rotation Radar: The RRR reveals TSM’s premium over the semiconductor basket remains elevated but is showing the first signs of exhaustion. The primary ratio (TSM/SMH) sits at 2.38, with the Fast MA falling below the Slow MA—an inversion suggesting the ratio spiked recently and is now decelerating, the momentum of outperformance fading even as the absolute premium persists. The secondary ratio (TSM/AVGO) shows TSM still commands a significant premium over the back-end leader, but this is precisely the spread the essay argues will compress as the market reprices forge versus armory. The ribbon in the top pane shows contested territory: green and red alternating through the autumn, with red now gaining persistence as 2026 begins. The regime color has shifted from deep amber dominance during the summer rally into a yellowing zone where leadership is no longer assured. The histogram bars show distribution beginning to appear in recent sessions, volume favoring the denominator over the numerator. The previously unknowable insight is timing: TSM has held its premium longer than the sector has held its bid, creating a divergence that must resolve—either TSM leads the sector back up, or TSM catches down to where the sector has already gone. The RRR suggests the latter is more probable, and the forge-to-armory rotation provides the fundamental catalyst for that compression.

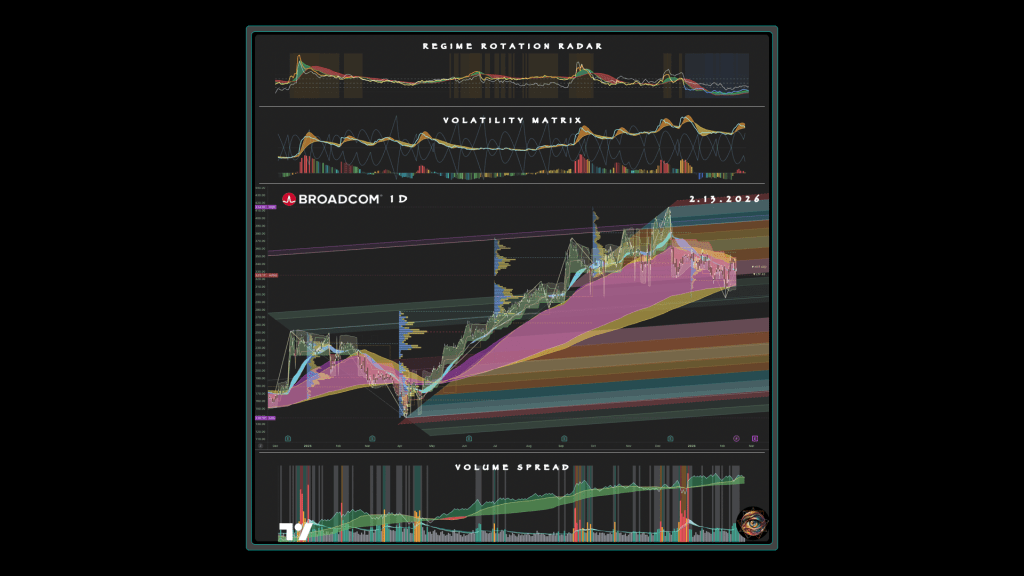

Trade 4: Broadcom as the Logistics-and-AI Compounder

The quietest chokepoints are often warehouses, not fabs.

AVGO may also be earlier in its cycle, potentially setting up for a turn while peers are already extended. Volume momentum has turned negative, a contrarian signal when price is approaching support rather than breaking down. Trend is absent—price is consolidating rather than collapsing. Bullish divergence hints at momentum bottoming even as price tests support. The overall picture is a stock washing out weak hands before the next leg, not a stock losing its fundamental bid.

Instrument: Broadcom Inc. (AVGO), long equity.

Thesis: Malaysian investment materials describe Broadcom’s Penang presence as a major global distribution and operations footprint, underscoring that Malaysia is not only manufacturing but also logistics coordination for global semiconductor flows. In a world paying for supply-chain optionality, the ability to ship from multiple nodes becomes strategic. AVGO’s Malaysia-tied logistics footprint functions as a hidden stabilizer while AI custom silicon keeps the upside convex.

Catalysts and Monitoring: March 6, 2026: AVGO earnings (monitor segment commentary on AI custom silicon and supply chain resilience). Subsequent quarterly earnings for confirmation of AI revenue trajectory and margin stability.

Entry / Exit Logic: Enter on a post-earnings gap that holds above the gap-day low for three sessions, or on a pullback that reclaims the rising fifty-day moving average with a high-volume reversal. Scale one-third at 2 R, trail the remainder using weekly higher lows. Time stop: twelve months if the relative-strength thesis does not materialize.

Invalidation: Weekly close below the ten-week moving average and a lower low versus the prior swing (one R). Earnings show AI growth decelerating materially while management highlights supply chain constraints or customer pushouts.

Risk Management: Risk one R maximum. Keep AVGO plus INTC combined semiconductor exposure hedged by Trade 2 during high-beta periods.

Price Action: AVGO peaked near $415 in late October and has since carved a wide range between $270 and $390, with current price at $329 sitting in the lower half of that range. The pitchfork structure from the 2024 lows shows price still respecting the broader uptrend channel, though it has pulled back to test the lower median lines after failing to hold the upper channel through December. The Periodic Volume Profile reveals heavy transaction volume in the $320–$360 zone from Q4, creating a shelf of support where buyers previously stepped in. The HTF and LTF markers both sit above current price, suggesting the pullback has room to base before the trend structure breaks.

Volume Spread Analysis: Volume on the recent decline has been lighter than average, running below both short and intermediate moving averages—a sign that sellers lack conviction rather than a sign of accumulation. On Balance Volume remains elevated and stable, with the short MA sitting above the long MA, indicating that institutional positioning has not yet shifted. The green shaded area in the cumulative flow pane continues to expand, suggesting underlying demand persists despite the price weakness. This is a stock pulling back within a trend, not a stock rolling over.

Volatility Matrix: Daily ranges have compressed recently, with realized volatility declining as the pullback matures and price approaches the support zone. The trend structure remains bullish, with the trend line at $365.57 as the level to reclaim and the anchor at current price—a close above that line would confirm the pullback is complete. The volatility stop at $327.31 sits just below current price, making this a decision point: hold here or accelerate lower. The projected limits at $329 and $344 bracket the immediate range, suggesting consolidation is the base case if support holds.

Regime Rotation Radar: The RRR reveals a stock that has underperformed the sector during the recent drawdown but is now approaching conditions where that underperformance may reverse. The primary ratio (AVGO/SMH) shows AVGO has lagged the semiconductor basket, yet the momentum lines are converging, suggesting the underperformance is decelerating. The secondary ratio (AVGO/NVDA) shows AVGO has lagged Nvidia as well, but by a narrower margin than it has lagged the sector, hinting that relative strength is emerging against the AI narrative leader specifically. The ribbon in the top pane has been contested throughout the autumn and winter, with neither green nor red establishing dominance—a regime in transition rather than a regime in collapse. The regime color has shifted into the red zone during the recent weakness, yet the depth of that red is shallow compared to prior troughs, suggesting sellers are exhausting. The cumulative flow pane shows the green area continuing to expand even as the ratio weakens, a divergence that favors the long thesis. The previously unknowable insight is this: AVGO’s underperformance has been a function of sector rotation rather than fundamental deterioration, and the RRR shows that rotation nearing its end—when the ratio inflects, the quiet chokepoint will be repriced as the market discovers that logistics and custom silicon compound while GPU narratives mean-revert.

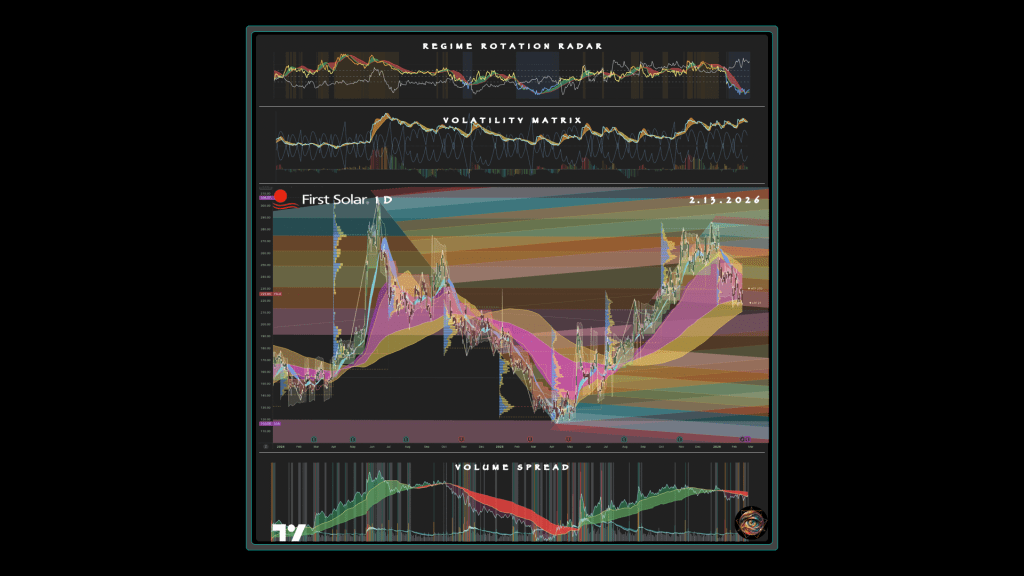

Trade 5: First Solar as the Electron Hedge

Chips do not care about your sustainability slide, yet procurement officers do.

FSLR may be another early mover if price holds support. Negative volume momentum is turning up after a period of decline, an early sign that buying interest may be returning. Bullish divergence hints at momentum stabilizing even as price tests the lower bound. A reversal of the down-trend here would carry conviction. The overall picture is a stock washed out by sector rotation, now approaching levels where risk-reward favors patience over aggression.

Instrument: First Solar, Inc. (FSLR), long equity.

Thesis: First Solar has a major manufacturing footprint in Kulim, Malaysia—the same region where Tenaga Nasional is committing tens of billions of ringgit to grid upgrades and where the Johor AI buildout is establishing the template for hyperscaler power demands. If Malaysia’s dirty-grid constraint becomes a binding limiter, demand for utility-scale solar rises—and FSLR’s non-China manufacturing positioning is a lever on that theme. The neutral wire still carries current from coal; the companies that can change that equation will be repriced.

Catalysts and Monitoring: Late February 2026: FSLR earnings (monitor bookings, average selling prices, and capacity commentary). Malaysia grid and transition cadence through 2026 (monitor Reuters energy coverage and Tenaga Nasional capex updates).

Entry / Exit Logic: Enter on a daily reclaim of the fifty-day moving average after earnings, or on a weekly higher-low hold at prior support with improving volume. Avoid catching falling knives. Scale one-third at 2 R, one-third at 3 R, trail the remainder. Time stop: twelve months.

Invalidation: Close below the most recent weekly swing low (one R). Evidence of sustained margin compression from pricing pressure and lack of demand pull from utility-scale projects.

Risk Management: Treat FSLR as a partial hedge to power-constraint risk in INTC and AVGO. Cap risk at 0.75 R if semiconductor exposure is already large.

Price Action: FSLR is a volatile stock that trades in wide ranges, with price swinging from $117 to $307 over the past two years. Current price at $203 sits in the middle of the recent range, having rallied sharply from the September 2025 low near $117 to a January 2026 high near $270 before pulling back. The pitchfork structures reveal a stock that respects channels during trends but breaks them violently during reversals—a pattern that rewards patience and punishes early entries. The Periodic Volume Profile shows heavy transaction volume in the $200–$230 zone, creating a shelf where the current pullback is finding support. The HTF marker sits higher near $270 while the LTF marker is at current price, suggesting the higher-timeframe trend remains intact but the lower-timeframe correction is still in progress.

Volume Spread Analysis: Volume on the pullback has been light, running below both short and intermediate averages—sellers lack conviction rather than buyers lacking interest. On Balance Volume has drifted lower with price but remains above its long moving average, indicating the underlying accumulation from the autumn rally has not been fully unwound. The cumulative flow pane shows the green area contracting modestly but not collapsing, a healthy correction within a trend rather than distribution. This is a stock resting after a strong move, not a stock losing its fundamental bid.

Volatility Matrix: Daily ranges have been stable, with realized volatility neither expanding nor compressing dramatically during the pullback. The trend structure has flipped cautiously bearish, with the trend line at $192.49 as nearby support and the anchor at $203.06 marking current price exactly—a decision point where bulls must hold or cede control. The volatility stop at $208.92 sits just above current price, suggesting the stock is testing the lower bound of its recent range. The projected limits at $207 and $217 bracket the immediate battleground, with a close above $209 needed to negate the short-term bearish setup.

Regime Rotation Radar: The RRR reveals a stock in deep underperformance that is now showing the first signs of regime transition—beaten down, but no longer accelerating lower. The primary ratio (FSLR/TAN) shows First Solar has significantly lagged the solar ETF, yet the momentum lines are attempting a bullish crossover, suggesting the worst of the relative weakness may be behind. The secondary ratio (FSLR/SPY) shows First Solar has also lagged the broad market, but by a wider margin than it has lagged its own sector—some of the weakness is market-driven rather than company-specific. The ribbon has spent months in red dominance as the stock corrected, but the most recent sessions show green beginning to contest for the first time since the decline began. The regime color sits in transition territory, no longer the deep blue of capitulation but not yet the amber of leadership—a stock in purgatory, waiting for a catalyst to tip the balance. The cumulative flow shows distribution giving way to accumulation, a structural shift that typically precedes price recovery by weeks or months. The previously unknowable insight is timing: FSLR’s underperformance was driven by sector rotation away from clean energy and toward AI, but the Malaysia grid constraint creates a fundamental catalyst that could reconnect the two narratives—when hyperscalers demand clean megawatts alongside clean rooms, the electron hedge becomes the AI trade by another name.

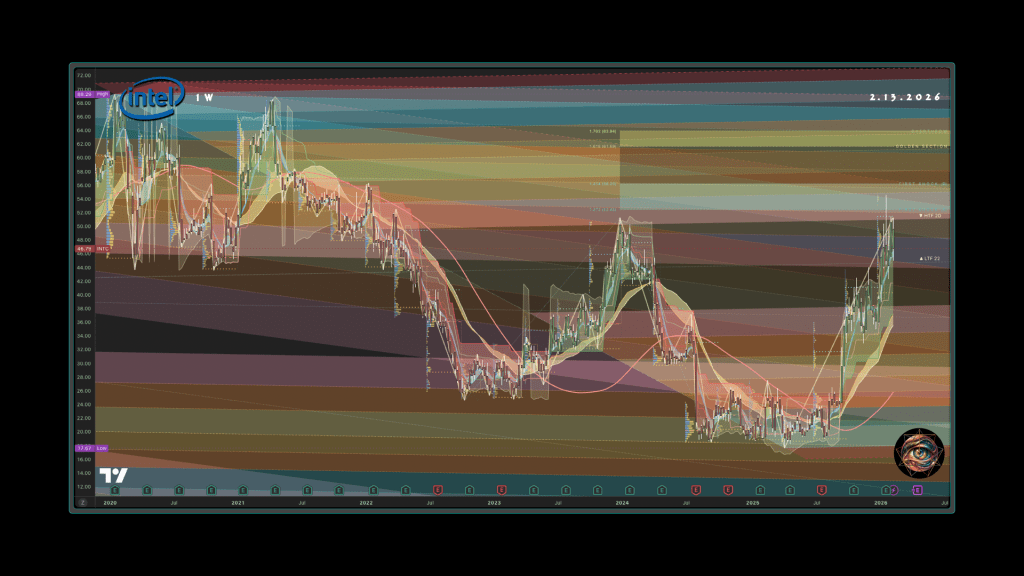

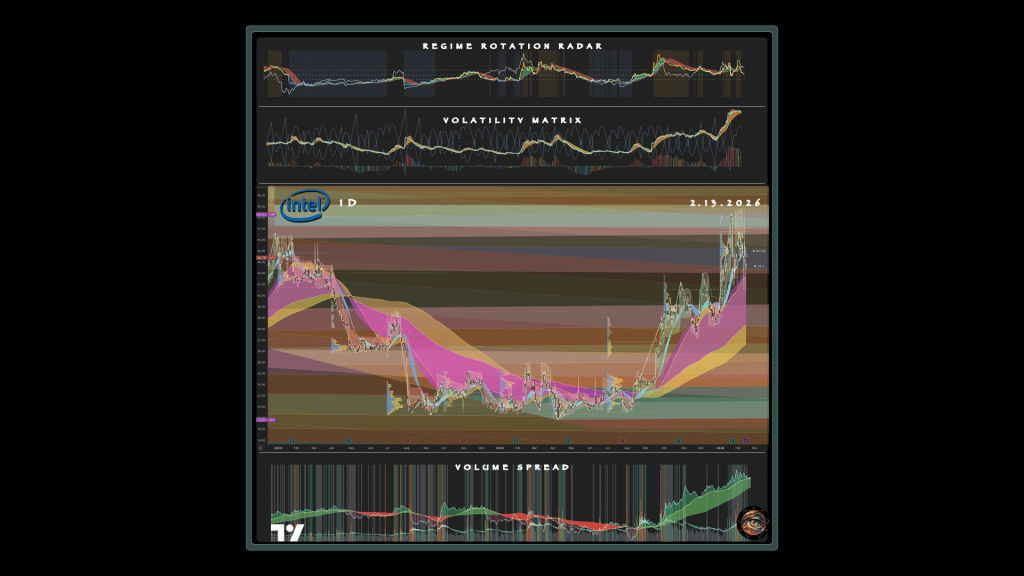

Trade 6: Intel as the Packaging Re-Rating Option

A turnaround sometimes hides inside a single facility that finally ships.

Based on a zoomed-out view, Intel appears mid-cycle rather than early—a turnaround already in progress, now being tested at a critical juncture. No directional bias leaves the stock open to resolution in either direction. Price is range-bound, coiling for its next move rather than trending up or down. No divergence means price and momentum align in indecision. The stock rests at an inflection point, where the next earnings cycle will determine whether the turnaround thesis survives or dies.

Instrument: Intel Corporation (INTC), long equity.

Thesis: Intel has publicly committed to invest up to seven billion dollars in Malaysia tied to advanced packaging, explicitly positioning Malaysia as its first overseas advanced packaging facility. If advanced packaging is a bottleneck, then capacity that actually ramps becomes a narrative catalyst. INTC can earn a multiple upgrade if Malaysia-linked packaging execution supports foundry and AI roadmaps.

Catalysts and Monitoring: April 2026 earnings window for updates on packaging and foundry execution. Malaysia NSS progress and anchor-investor updates through 2026–2027 (monitor MITI and MIDA releases for project milestones).

Entry / Exit Logic: Enter on a weekly close above the most recent earnings-reaction high, or on a post-pullback reclaim of the two-hundred-day moving average with improving relative strength versus SOXX. Scale fifty percent at 2 R, trail the remainder on weekly higher lows. Time stop: eighteen months if the re-rating does not appear.

Invalidation: Weekly close below the prior major swing low (one R). Credible reporting or company disclosure of Malaysia packaging delays or underutilization.

Risk Management: Size to 0.75 to 1.0 R risk. Keep sector-level drawdown bounded using Trade 2.

Price Action: Intel has been a falling knife for years, declining from $69 in 2021 to a low of $17.67 in late 2024—a destruction of shareholder value that left the stock for dead in most portfolios. The rally from that low to $54.60 in early 2025, followed by another collapse to $18 and then a second rally to $54.60 in January 2026, has created a massive basing pattern visible on the weekly chart. Current price at $20.25 sits near the bottom of the range, having given back nearly all of the recent gains. The pitchfork structures show price oscillating between extremes, respecting neither trend nor range for long—a stock that punishes conviction in either direction. The Periodic Volume Profile reveals heavy transaction volume in the $20–$25 zone, a battleground where buyers and sellers have fought repeatedly over the past two years.

Volume Spread Analysis: Volume has been elevated during both rallies and declines, reflecting high interest in the turnaround narrative even as execution disappoints. On Balance Volume shows a long base-building process, with modest distribution recently but no collapse in the underlying accumulation structure. The cumulative flow pane shows the green area expanding since the 2024 low, indicating accumulation despite the volatile price action. This is a stock being repositioned by patient capital, not abandoned.

Volatility Matrix: Daily ranges have compressed recently as the stock consolidates near the lower bound of its range, a coiling that typically precedes directional resolution. The trend structure is neutral, with the trend line and anchor both sitting just above current price—price is testing whether support holds or fails. The volatility stop at $21.26 marks the level that must be reclaimed to shift momentum. The projected limits bracket a narrow range, suggesting the stock is wound tight and waiting for a catalyst.

Regime Rotation Radar: The RRR reveals a stock that has been in persistent underperformance but is now approaching a potential regime inflection—still lagging, but lagging less aggressively than before. The primary ratio (INTC/SOXX) shows Intel significantly behind the semiconductor index, yet the momentum lines are converging rather than diverging, suggesting the worst of the relative weakness may be decelerating. The secondary ratio (INTC/AMD) shows Intel continues to lag its direct competitor, but the ribbon has shifted from sustained red dominance into contested territory for the first time in months. The cumulative flow tells a different story than price alone: accumulation has expanded steadily since mid-2024, even as price has whipsawed, indicating that institutional capital is building positions through the volatility rather than fleeing. The regime color sits in deep blue territory, the zone of capitulation where stocks are priced for permanent impairment—yet the ribbon contesting and flow accumulating suggest the market may be mispricing the turnaround. The previously unknowable insight is optionality: Intel’s stock price reflects execution failure across multiple fronts, yet the Malaysia packaging facility represents a single point of potential success that is not in the price—if that facility ships on time and at yield, the re-rating will be violent, because the market has already priced in the opposite outcome.

Portfolio Overlay

These setups cluster around a single idea: the AI-era semiconductor stack is constrained by more than front-end fabs. Packaging, power semiconductors, logistics, and electricity are all potential bottlenecks, and Malaysia sits at the intersection of several.

De-risk the basket by sizing each position to its R budget, treating INTC, AVGO, and NVDA exposure as a single correlated block. The shared risks are threefold. A broad semiconductor drawdown spikes correlations and punishes all positions simultaneously. Policy shocks—export controls, subsidy shifts, geopolitical escalation—can invalidate individual theses overnight. Power and permitting delays slow real-world deployment and erode the upgrade narrative.

Use the SMH put spread as the explicit circuit breaker when the market stops rewarding nuance. Enter only when the regime aligns with the thesis. Exit when divergence signals exhaustion or transition.

The armorers are still at their stations. The travelers are still crossing. These trades speculate on the crossing remaining passable long enough for the village to upgrade—and hedge against the possibility that it does not.

Leave a comment