Executive Summary

SpaceX is a vertically integrated aerospace, satellite-connectivity, and AI-infrastructure company headquartered in Hawthorne, California, trading on Nasdaq under the ticker SPCX following a record-setting June 12, 2026 IPO. The business now runs as three reported segments: Space (Falcon/Starship launch services), Connectivity (Starlink), and AI (the former xAI, including Grok and X), with Connectivity generating the substantial majority of consolidated operating profit and AI generating the substantial majority of consolidated losses. 2025 consolidated revenue was $18.674 billion (33% YoY growth) against a GAAP net loss of $4.94 billion and adjusted EBITDA of $6.584 billion, a gap driven primarily by AI-segment losses and Starlink depreciation rather than by the launch business. The company carries an unusually founder-favorable governance structure (Class B shares carrying ten votes each, Musk at ~85.1% voting power, Texas reincorporation, mandatory arbitration, a 3% derivative-suit threshold) that drew formal objection from the NYC and NYS Comptrollers, CalPERS, and the Council of Institutional Investors. Top near-term risks: AI-segment unit economics, the staggered post-IPO lockup calendar running through Musk’s 366-day personal lockup in June 2027, launch-market competition from Rocket Lab and Blue Origin, and a valuation that already prices in execution across all three business lines simultaneously.

SpaceX’s First Week Already Knows Its Own Future

Homepage

Perplexity Finance Page

TradingView

Overview & Business Segments

SpaceX was founded in 2002 by Elon Musk to reduce launch costs and enable Mars colonization via reusable rockets and spacecraft; headquarters sit in Hawthorne, California, with major operations at Starbase (Texas), Cape Canaveral (Florida), and Vandenberg (California). The stated mission remains “to make humanity multiplanetary,” though the current revenue mix is driven primarily by terrestrial connectivity and AI compute rather than spaceflight itself.

- Space segment (Falcon 9, Falcon Heavy, Starship): 2025 revenue $4.086 billion; the segment has completed roughly 650 missions to date, with more than 95% of 2025 launches using a previously flown booster. Q1 2026 segment revenue was $619 million against a segment EBITDA loss of $351 million.

- Connectivity segment (Starlink): 2025 revenue $11.387 billion (61% of consolidated revenue), operating income $4.423 billion, adjusted EBITDA $7.168 billion (+86.2% YoY); more than 9,600 satellites deployed and 10.3 million subscribers across 164 countries as of Q1 2026. Average revenue per user slipped from $81 (end of 2025) to $66 (Q1 2026) as Starlink expanded into lower-priced international markets.

- AI segment (xAI/Grok/X, acquired into SpaceX February 2, 2026; X itself was acquired by xAI in March 2025 and consolidated retroactively): 2025 revenue $3.201 billion against an operating loss of $6.355 billion, the dominant driver of the company’s consolidated net loss.

- On June 16, 2026, SpaceX announced a pending $60 billion all-stock acquisition of Anysphere (maker of the Cursor AI coding assistant), expected to close Q3 2026; Morningstar estimated roughly 3.4% dilution to IPO-era equity from the deal and cut its fair-value estimate to approximately $62 per share following the announcement.

Leadership & Governance

Elon Musk is CEO, CTO, and Chair. The board blends long-tenured engineering leadership with representatives of major pre-IPO investors (Founders Fund, DFJ, and others); the company qualifies for and uses Nasdaq’s “Controlled Company” exemption, which removes the independent-board-majority requirement a normal listed company would face.

- Capital structure: Class A shares (sold to the public) carry one vote each; Class B shares carry ten votes each. Total shares outstanding post-IPO are approximately 13.08 billion (7.38B Class A, 5.70B Class B). Musk holds roughly 42% of total equity and approximately 85.1% of voting power.. SpaceX’s charter reportedly requires Musk’s own consent for his removal as CEO.

- Reincorporation and forum: SpaceX reincorporated from Delaware to Texas in February 2024. Bylaws route shareholder disputes to the Texas Business Court, impose mandatory arbitration on securities-law claims (eliminating class-action exposure on those claims), and set a 3% ownership threshold both for bringing a derivative suit and for submitting a shareholder proposal (the latter also requiring a six-month holding period and solicitation of holders representing 67% of voting power). At the IPO valuation, the 3% derivative threshold requires a position worth tens of billions of dollars to exercise.

- Formal objections: A May 13, 2026 joint letter from NYC Comptroller Mark Levine, NYS Comptroller Thomas DiNapoli, and CalPERS CEO Frost called the governance package “novel and extreme” and asked SpaceX to drop the arbitration clause and the 3% threshold.A separate June 9, 2026 letter from the Council of Institutional Investors raised substantially the same objections.

- Cross-holdings: Tesla’s Q1 2026 filing disclosed a $2 billion equity investment in SpaceX. Unconfirmed market speculation (Wedbush analyst Dan Ives, no on-the-record company statement) has floated a possible SpaceX–Tesla combination, contingent on a Tesla compensation-plan trigger tied to a $7.5 trillion combined market cap; treat as rumor, not fact, pending any official disclosure.

Market Position & Competitors

SpaceX performs roughly five of every six US orbital launches (estimates range 83–87%), giving it a near-monopoly position that has drawn academic and policy attention to launch-market concentration. Competitive pressure is building from several directions rather than any single rival:

- Launch: Rocket Lab (RKLB), scaling its Neutron medium-lift vehicle toward direct Falcon 9 competition; Blue Origin, transitioning from development to operational cadence; traditional primes (Lockheed Martin, Boeing) and ULA, less competitive on price and cadence but politically entrenched.

- Connectivity: OneWeb/Eutelsat in select regions and enterprise segments; Amazon’s Kuiper constellation as a medium-term consumer/enterprise rival.

- AI: OpenAI and Anthropic, both with stronger current enterprise penetration than xAI/Grok; notably, both Alphabet (~$30 billion cloud-compute deal running through mid-2029) and Anthropic (~$45 billion compute agreement spanning roughly three years) are simultaneously SpaceX AI-infrastructure customers, which is worth flagging as a related-party-adjacent revenue dynamic rather than purely arm’s-length demand.

Financials & Capital Structure

The S-1 reports a Q1 2026 operating loss of $1.943 billion against EBITDA of $1.127 billion; several secondary outlets separately reported a Q1 2026 “net loss” of $4.28 billion on the same $4.694 billion revenue figure. The gap between the filed operating-loss figure and the widely circulated net-loss figure was not reconciled in this pass and should be checked against the actual 10-Q before being treated as settled.

- Debt: A $20 billion bridge loan (arranged by Goldman Sachs, Bank of America, Citigroup, JPMorgan, and Morgan Stanley) retired $17.5 billion of X/xAI junk debt that had carried rates up to 12.5%, cutting the effective rate to 4.58% as of March 31, 2026. Total long-term debt stood at $29.1 billion as of that date. SpaceX announced a $20 billion investment-grade bond offering on June 18, 2026 (Moody’s Baa1, Fitch BBB+, S&P BBB) to refinance the bridge loan ahead of its September 2027 maturity.

- Other balance-sheet items: SpaceX disclosed holding 18,712 Bitcoin, acquired for roughly $661 million, marked at approximately $1.29 billion as of March 31, 2026.

- Pre-IPO capital: More than $10 billion raised in venture funding prior to listing; disclosed backers include Founders Fund, DFJ, D1 Capital, Fidelity, Thrive Capital, Craft Ventures, and Adapt Ventures.

- TAM claim: SpaceX’s own S-1 frames its addressable market at $28.5 trillion; this is a company-sourced figure, not an independent estimate, and should be cited as such.

Public Market Information & Valuation

SpaceX priced its IPO at $135 per share on June 12, 2026, selling 555.6 million shares to raise $75 billion at an offer-stage valuation near $1.75–1.77 trillion; lead underwriters were Goldman Sachs and Morgan Stanley, alongside BofA Securities, Citigroup, and JPMorgan among 21 total banks in the syndicate. Shares closed the first session at approximately $161 (+19.3%), implying a market cap near $2.1 trillion. Chinese and Hong Kong investors were barred from participating in the offering.

- Float and lockup: Roughly 4–5% of total shares were tradeable at listing. The remaining 180-day block releases in stages: 20% on Q2 2026 earnings (with a conditional additional 10% if SPCX trades at or above $175.50 — 30% over the IPO price — for 5 of the 10 trading days preceding that earnings date), then 7% tranches at fixed dates through August–October, then 28% on Q3 2026 earnings, with the remainder releasing at the full 180-day mark (December 8, 2026). Musk’s roughly 6.4 billion shares are locked for 366 days with no early-release provision, first eligible June 12, 2027; a separate “extended investor” group unlocks into 2027 as well.

- Index treatment: Nasdaq adopted a fast-entry rule permitting inclusion within 15 trading days rather than the standard quarterly review; Russell similarly adjusted its rules. The S&P 500 declined to include SpaceX as of its June 4, 2026 review, citing standard eligibility criteria.

- Derivative products and proxies: ProShares launched a 2x daily leveraged ETF (SPCF) on SpaceX’s listing day. EchoStar (SATS) holds an equity stake exceeding 2% in SpaceX, acquired via 2025 spectrum-for-equity transactions valued at roughly $11–17 billion at signing; post-IPO mark-to-market estimates for that stake range from approximately $27 billion to $44 billion depending on which SpaceX valuation is applied — this figure is genuinely unsettled across sources and should not be cited as a single number.

- Retail allocation: Approximately 30% of the offering (roughly $22.5 billion) was allocated to individual investors, routed through Robinhood, Fidelity, and Charles Schwab.

- Forward valuation estimates (both from deal underwriters, note the conflict of interest): Morgan Stanley projects $3.4 trillion revenue and $2.7 trillion adjusted EBITDA by 2040 ($330B revenue / $190B AI revenue by 2030); Goldman Sachs projects a more bullish ~$470 billion total revenue by 2030 ($322B from AI). Both projections lean heavily on AI-segment growth assumptions that are, as of this writing, unproven at scale.

- Independent bear case: Morningstar’s fair-value estimate sits near $62 per share, well below both the $135 IPO price and subsequent trading levels, following the Anysphere/Cursor acquisition announcement.

Strategic, Regulatory & Risk Factors

- Antitrust / market concentration: SpaceX’s roughly 83–87% share of US orbital launches has drawn policy-research attention (CSET) to concentration risk in a market the government simultaneously depends on for national-security launch.

- Export controls: As a US aerospace and defense contractor, SpaceX operates under ITAR, limiting business in certain regions.

- Geopolitical exposure: Starlink’s coverage decisions in active conflict zones have drawn public scrutiny and calls for clearer governance over who controls connectivity in a war zone.

- Key-person risk: Musk simultaneously leads SpaceX, Tesla, X, xAI, Neuralink, and The Boring Company; governance documents concentrate enough control in his hands that this risk cannot be mitigated by ordinary board action (see Section 2).

- Litigation/governance risk: The Texas venue, mandatory arbitration, and 3% derivative threshold together narrow practical shareholder recourse to entities large enough to clear that threshold alone, which functionally excludes most individual holders (see Section 2).

- Execution risk: AI-segment unit economics remain unproven against $190–322 billion 2030 revenue assumptions baked into underwriter valuations; launch-market margin compression as Rocket Lab and Blue Origin reach operational scale; Starlink ARPU pressure from international expansion.

Telecom Peers

EchoStar Corporation (SATS) – EchoStar operates satellite communications and broadband businesses (notably Hughes), but its equity narrative in 2026 is dominated by its sizable minority stake in SpaceX acquired through strategic transactions and legacy DISH structures. That stake, estimated around low‑single‑digit ownership, now represents a significant portion—sometimes more than—EchoStar’s own market capitalization, effectively making SATS a leveraged indirect way to own SPCX while also holding spectrum, satellite assets, and subscriber relationships. The company is working through integration, cost‑takeouts, and spectrum monetization to stabilize cash flow after years of disruption in pay‑TV and GEO broadband. Strategic risks include execution on debt reduction in a rising‑rate environment, secular decline in legacy video/broadband businesses, and correlation risk: SATS can trade more like a volatile proxy for SpaceX than on its own fundamentals. Regulatory decisions on spectrum sharing, rural broadband subsidies, and competitive pressure from fiber and LEO offerings (including Starlink itself) are additional pressure points.

AST SpaceMobile, Inc. (ASTS) – AST SpaceMobile is building a direct‑to‑device cellular broadband network using large LEO satellites designed to connect directly to standard smartphones without special hardware. It has signed framework agreements and MOUs with major mobile network operators worldwide, positioning itself as a wholesale extension of terrestrial LTE/5G coverage in rural and oceanic areas. The company recently launched next‑generation BlueBird satellites on Falcon 9 and secured key FCC approval for US direct‑to‑device service, validating aspects of the technology and regulatory story. Its relative position is as a pure‑play D2D satellite‑cellular name, potentially complementary to incumbents like Iridium but more aggressive on bandwidth and smartphone integration. Strategic risks are substantial: heavy capital needs, dependence on successful multi‑satellite deployments, and the need to convert MOUs into high‑margin recurring revenue before funding windows narrow. Competitive threats include terrestrial operators’ own NTN plans, SpaceX/partnered initiatives, and evolving spectrum/standardization outcomes that could favor rival architectures.

Iridium Communications Inc (IRDM) – Iridium operates the world’s only truly global narrowband LEO satellite network, delivering voice, data, and emerging positioning, navigation and timing (PNT) services to aviation, maritime, government, and industrial users. Its relative position is as the incumbent provider of mission‑critical, low‑bandwidth connectivity where coverage and reliability trump throughput, underpinned by long‑term US government and defense relationships and scarce L‑band spectrum. The 2025–2026 outlook shows modest service‑revenue guidance—flat to up 2%—with strong OEBITDA and cash generation but a tempered growth story, shifting investor focus to new IoT, NTN Direct, and PNT offerings that could unlock incremental revenue later in the decade. Strategic challenges include saturation in legacy maritime and equipment revenue, competitive encroachment from higher‑throughput LEO constellations and 3GPP‑aligned NTN solutions, and the need to fund future constellation refreshes. If Iridium can successfully commercialize IoT and PNT while defending its government niche, it remains a durable cash‑flow compounder; if not, it risks being overshadowed by broadband‑centric peers.

PLDT Inc. Sponsored ADR (PHI) – PLDT is the oldest and largest integrated telecom operator in the Philippines, with leading fixed‑line and fiber broadband positions and a major share of the mobile market. Its core offerings span mobile voice/data, home fiber, enterprise connectivity, data centers, and digital platforms, supported by an extensive national network. Strategically, PLDT is leaning into fiber and 5G deployment, fintech and enterprise ICT, positioning itself as the backbone of the Philippines’ digital‑economy growth while optimizing its tower and data‑center portfolios. However, management itself has warned that new policies—covering pricing, infrastructure‑sharing, and quality‑of‑service obligations—risk compressing margins in an already saturated market. Key risks include regulatory intervention on tariffs and competition, high ongoing capex requirements, FX and macro volatility, and the need to maintain credibility after past capex accounting issues. Balancing network investment with dividends and deleveraging remains a central strategic challenge.

Ituran Location and Control Ltd. (ITRN) – Ituran is a telematics and location‑based services provider offering stolen‑vehicle recovery, fleet management, connected‑car services, and mobile asset tracking, primarily in Israel and Brazil with growing international reach. The business is driven by recurring subscription revenue—around three‑quarters of sales—complemented by hardware product revenue, giving it an attractive service margin profile and strong cash generation. Strategically, Ituran is repositioning from a traditional SVR provider to a broader connected‑mobility and data platform, monetizing analytics and value‑added services for insurers, auto lenders, OEMs, and fleet operators. Its relative position is strong in core markets, with entrenched insurer partnerships and brand recognition, but it competes in a fragmented global telematics space against larger, better‑capitalized peers. Key risks include exposure to cyclical auto sales and credit conditions, regulatory shifts in insurance and privacy, FX and political risk in Latin America and Israel, and potential commoditization of basic tracking as OEM‑embedded connectivity becomes standard.

Telesat Corporation (TSAT) – Telesat is a Canadian satellite operator transitioning from a shrinking geostationary (GEO) video and data business to Telesat Lightspeed, a planned enterprise‑ and government‑focused LEO constellation. Lightspeed is designed around high‑throughput, low‑latency broadband with specialized features for defense and sovereign customers, including dedicated military Ka‑band capacity and integration into Canada’s ESCAPE defense communications program. The company has secured multi‑billion‑dollar funding and a multi‑launch Falcon 9 contract with SpaceX to deploy the constellation starting in 2026, targeting global service entry around 2028. Its current challenge is bridging a period of declining GEO revenues—2025 revenue down roughly a quarter, EBITDA nearly halved—while financing and executing Lightspeed without over‑leveraging the balance sheet. Strategic risks center on schedule and capex creep, terminal ecosystem and landing‑rights build‑out, and competition from larger LEO players like SpaceX and OneWeb. Successful government and enterprise uptake could, however, reposition Telesat as a key sovereign‑secure LEO provider rather than a legacy video satellite operator;

iQSTEL Inc. (IQST) – iQSTEL is a global telecommunications and technology company offering wholesale and enterprise connectivity, messaging, and increasingly fintech, AI‑enabled telecom services, cybersecurity, and digital health solutions. Its revenue base is still roughly 80–87% telecom carriage and messaging, but fintech (via GlobeTopper) and digital services now contribute a growing minority and higher margin share. Q1 2026 revenue of about 97.9M, up nearly 70% year‑over‑year, and a full‑year target around 430M underscore a high‑growth profile, though gross‑margin expansion is more modest. Management’s strategy emphasizes consolidating telecom operations across almost 30 countries while scaling higher‑margin fintech, cybersecurity and AI offerings, and pursuing an eventual 1B revenue run‑rate and recurring dividends. Strategic risks include execution on integration and customer acquisition, vendor and platform dependence, working‑capital needs in a low‑margin wholesale environment, and dilution or governance concerns typical of rapid‑growth small caps.

Powell Max Limited (PMAX) – Powell Max is a micro‑cap holding and financial communications services company incorporated in the British Virgin Islands with operations centered in Hong Kong and a US presence in Florida. It historically provided financial printing, corporate reporting, translation, and related services for Hong Kong–listed and pre‑IPO companies, but is now repositioning as a diversified Nasdaq holding vehicle targeting cash‑flowing assets such as Boston Solar. Management has raised new capital, overhauled the board, completed a reverse share split, and articulated a plan to roll up high‑potential businesses while using capital‑markets access as a competitive edge. Its relative position is early‑stage and highly speculative, with a tiny market cap and limited operating scale compared to established diversified holdcos. Strategic risks include integration and execution on acquisitions, regulatory and governance scrutiny in both Hong Kong and US markets, financing risk in volatile small‑cap conditions, and potential misalignment between legacy print operations and new energy/industrial assets.

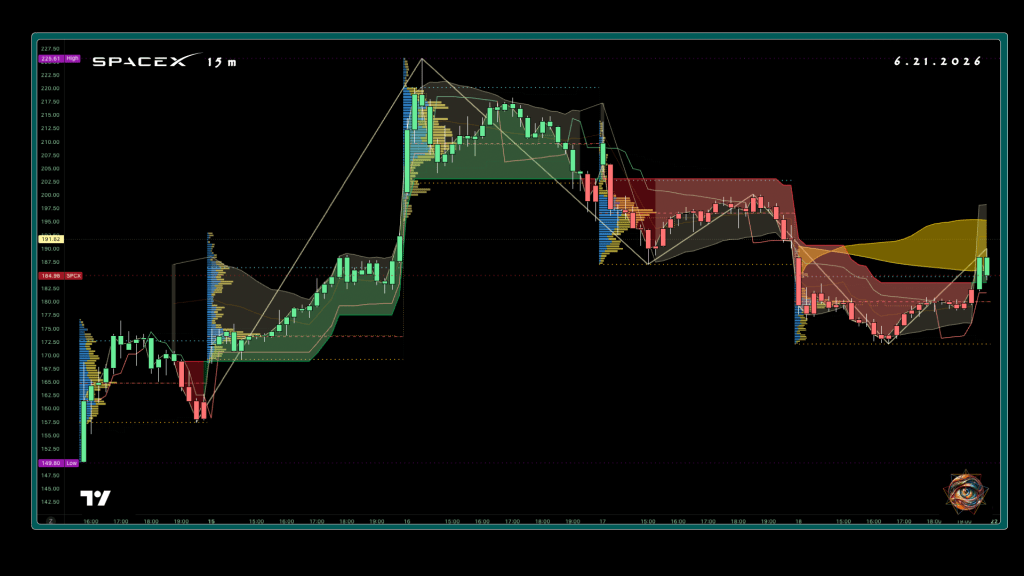

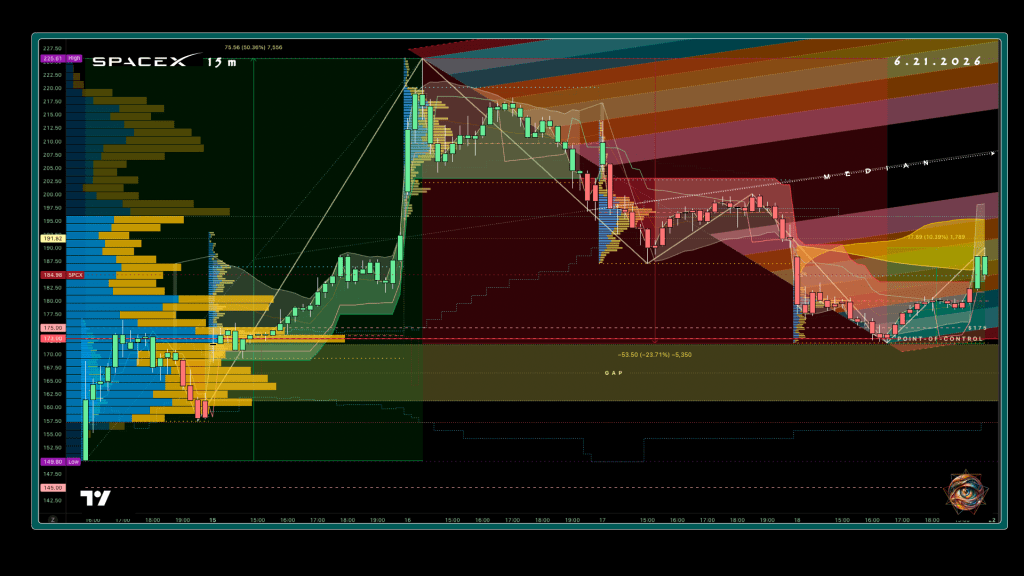

Appendix: Charts

6.21.2026—These charts track the first week of SPCX price action, as described.

Figure 1. SPCX (15m) – Week One Price Action, w/ SUPeR TRenD + Daily Volume Profiles – 6.21.2026

Figure 2. SPCX (15m) – Week One Price Action, w/ FibFork + Unit Volume Profile – 6.21.2026

Figure 3. SPCX (1m) – Week One Price Action, w/ Volatility Matrix + Volume Spread – 6.21.2026

Sources

[1] SpaceX Overview — https://rocketlaunch.org/launch-providers/spacex

[2] SpaceX files IPO prospectus — https://finance.yahoo.com/markets/article/spacex-files-ipo-prospectus-offering-a-peek-into-its-finances-205406189.html

[3] 6 Charts on SpaceX’s Pre-IPO Financials — Morningstar — https://www.morningstar.com/stocks/6-charts-spacexs-s-1-financials

[5] SpaceX Aims To Be the Largest IPO Ever — Yahoo Finance — https://finance.yahoo.com/markets/stocks/articles/spacex-aims-largest-ipo-ever-154919249.html

[6] The SpaceX IPO Prospectus: 15 Key Insights — Trending Topics — https://www.trendingtopics.eu/the-spacex-ipo-prospectus-15-key-insights-from-the-s-1-filing/

[7] Space Exploration Technologies S-1 — SEC EDGAR — https://www.sec.gov/Archives/edgar/data/1181412/000162828026036936/spaceexplorationtechnologi.htm

[8] SpaceX IPO: 5 Key Takeaways — Seeking Alpha — https://seekingalpha.com/article/4909346-spacex-ipo-5-key-takeaways-from-s1-filing-and-how-to-get-exposure-with-agix

[9] Space Exploration Technologies S-1/A#2 — SEC EDGAR — https://www.sec.gov/Archives/edgar/data/1181412/000162828026040364/spaceexplorationtechnologib.htm

[10] SpaceX (SPCX) Lockup Schedule — PurePowerPicks — https://purepowerpicks.com/spacex-lockup-schedule/

[11] SPCX Lockup & Vesting Tracker — Tokenomist — https://tokenomist.ai/stock/spcx

[12] How SpaceX’s Tiered Lockup Aims to Help Post-IPO Trading — Morningstar — https://www.morningstar.com/stocks/how-spacexs-tiered-lockup-aims-help-post-ipo-trading

[13] SpaceX SPCX Lock-Up Expiration Dates — StockAlarm Pro — https://pro.stockalarm.io/blog/spacex-ipo-lockup-financials

[14] SpaceX / SPCX Lock-Up Expiration Schedule 2026–2027 — BiyaPay — https://www.biyapay.com/en/blogdetail/4087-spacex-spcx-lockup-expiration-schedule-20262027-fl

[15] SpaceX Stock’s Lockup: You’ve Been Warned — Trefis — https://www.trefis.com/stock/spcx/articles/601883/spacex-stocks-lockup-youve-been-warned/2026-06-08

[16] SpaceX IPO Explained: SPCX, Lockup & Day 1 — StockCram — https://www.stockcram.com/blog/spacex-ipo-explained

[18] SpaceX IPO Index Inclusion — SpotGamma — https://spotgamma.com/spacex-ipo-index-changes-spotgamma/

[19] ProShares Launches SPCF ETF — https://www.proshares.com/press-releases/proshares-launches-spcf-etf-targeting-2x-daily-returns-of-spacex

[20] EchoStar (SATS) Stock: Your Gateway to SpaceX — Parameter — https://parameter.io/echostar-sats-stock-your-gateway-to-spacex-before-the-blockbuster-ipo/

[21] EchoStar Stock (SATS) Jumps 543% — TECHi — https://www.techi.com/echostar-stock-spacex-backdoor/

[22] EchoStar: There’s More To This Company Than Just SpaceX Shares — Seeking Alpha — https://seekingalpha.com/article/4898945-echostar-stock-there-is-more-to-this-company-than-just-spacex-shares

[23] SpaceX bridge loan cuts Musk’s debt costs in half — The Next Web — https://thenextweb.com/news/spacex-bridge-loan-musk-debt-refinancing-ipo

[24] SpaceX prepares $20 billion bond sale — Cryptopolitan — https://www.cryptopolitan.com/spacex-20-billion-bond-sale-xai-debt/

[25] SpaceX Stock Sheds $620 Billion in Two Sessions — TechTimes — https://www.techtimes.com/articles/318677/20260619/spacex-stock-sheds-620-billion-two-sessions-bond-deal-reveals-debt-deadline.htm

[26] SpaceX is seeking $20B in debt — TechFundingNews — https://techfundingnews.com/spacex-20b-investment-grade-debt-ipo-refinance-xai-acquisition/

[27] SpaceX plans $20B bond deal, reveals Bitcoin holdings — CryptoBriefing — https://cryptobriefing.com/spacex-20b-bond-deal-bitcoin-holdings/

[28] Elon Musk’s SpaceX Refinances Debt With $20 Billion Bridge Loan — Yahoo Finance — https://finance.yahoo.com/markets/stocks/articles/elon-musks-spacex-refinances-debt-163207330.html

[29] SpaceX and the New Geography of Corporate Governance — Truth on the Market — https://truthonthemarket.com/2026/06/03/spacex-and-the-new-geography-of-corporate-governance/

[31] Letter to SpaceX re: IPO — NYC Comptroller — https://comptroller.nyc.gov/reports/letter-to-spacex-re-ipo-from-nyc-comptroller-levine-nys-comptroller-dinapoli-and-calpers-ceo-frost/

[32] SpaceX IPO: Corporate Governance and Capital — Klover.ai — https://www.klover.ai/spacex_ipo_corporate_governance_and_capital_indepth_analysis_2026/

[33] CII Joint Letter to SpaceX — Maryland Comptroller (hosting) — https://www.marylandcomptroller.gov/content/dam/mdcomp/md/com-docs/06-09-2026-cii-letter-to-spacex.pdf

[34] SpaceX Maps Texas Strategy to Dodge Securities Class Actions — Bloomberg Law — https://news.bloomberglaw.com/legal-exchange-insights-and-commentary/spacex-maps-texas-strategy-to-dodge-securities-class-actions

[36] Morgan Stanley Forecasts Massive Revenue Expansion — Yahoo Finance — https://finance.yahoo.com/markets/stocks/articles/morgan-stanley-forecasts-massive-revenue-165800943.html

[37] SPCX IPO: Morgan Stanley Sees SpaceX Revenue Soar 182-Fold — Stocktwits — https://stocktwits.com/news-articles/markets/equity/spacex-revenue-soar-182-fold-3-4-trillion-2040-morgan-stanley-spcx-ipo/cZ0FkkIReCJ

[38] Morgan Stanley projects SpaceX revenue to reach $3.4T by 2040 — CryptoBriefing — https://cryptobriefing.com/morgan-stanley-spacex-revenue-3-4-trillion-2040/

[39] Morgan Stanley Sees SpaceX’s Revenue Reaching $3.4 Trillion — Yahoo Finance/Reuters — https://finance.yahoo.com/markets/stocks/articles/morgan-stanley-sees-spacex-revenue-112500980.html

[40] Shaping the U.S. Space Launch Market — CSET Georgetown — https://cset.georgetown.edu/publication/shaping-the-u-s-space-launch-market/

[41] EchoStar Stock Rockets As Massive $17 Billion Spectrum Deal — TIKR — https://www.tikr.com/blog/echostar-nasdaq-sats-stock-rockets-as-massive-17-billion-spectrum-deal-ties-company-to-highly-anticipated-spacex-public-debut

[43] SpaceX plans $20B bond deal, 18,712 Bitcoin disclosed — CryptoBriefing — https://cryptobriefing.com/spacex-20b-bond-deal-bitcoin-holdings/

[44] Elon Musk’s SpaceX Refinances Debt — Tesla $2B investment note — Yahoo Finance — https://finance.yahoo.com/markets/stocks/articles/elon-musks-spacex-refinances-debt-163207330.html

[46] SpaceX S-1 Ranks as Most Read Book on Wall Street — Gladstone Place Partners — https://www.gladstoneplace.com/news/spacex-s-1-ranks-as-most-read-book-on-wall-street-since-too-big-to-fail/

[50] SpaceX Maps Texas Strategy (derivative threshold dollar figure) — Bloomberg Law — https://news.bloomberglaw.com/legal-exchange-insights-and-commentary/spacex-maps-texas-strategy-to-dodge-securities-class-actions

[51] SpaceX is about to go public — least shareholder-friendly — Fortune — https://fortune.com/2026/05/22/space-x-stock-ipo-price-elon-musk-shareholders/

[56] Morgan Stanley Sees SpaceX’s Revenue Reaching $3.4 Trillion in 2040 — original WSJ-sourced piece — https://finance.yahoo.com/markets/stocks/articles/morgan-stanley-sees-spacex-revenue-112500980.html

[58] Space Exploration Technologies S-1 (financial tables) — SEC EDGAR — https://www.sec.gov/Archives/edgar/data/1181412/000162828026036936/spaceexplorationtechnologi.htm

[59] Morgan Stanley projects SpaceX revenue — roadshow/IPO terms detail — CryptoBriefing — https://cryptobriefing.com/morgan-stanley-spacex-revenue-3-4-trillion-2040/

[60] Morgan Stanley Sees SpaceX Revenue Reaching $3.4 Trillion — banker fee/role detail — Yahoo Finance — https://finance.yahoo.com/markets/stocks/articles/morgan-stanley-sees-spacex-revenue-112500980.html

Leave a comment